The 4% Rule Is a Guess (And That's Fine)

Everyone in the FIRE community treats it like scripture. It's actually a back-of-the-envelope calculation from 1994. Here's why I use it anyway.

There's a moment in every early retiree's journey -- usually around 3 AM, usually alone, usually with too many browser tabs open -- when the euphoria of the savings rate discovery hardens into a different question. A colder one.

Okay, I can save enough. But how do I know I won't run out?

I remember exactly where I was. Kitchen table, San Miguel de Allende, three weeks after we'd landed. The spreadsheet that had set me free -- the one I wrote about in The Math That Changed Everything -- was still open. But I wasn't looking at the accumulation side anymore. I was looking at the other direction. The drawdown. The decades-long slow bleed of a portfolio that had to feed a family of three for what I hoped would be a very, very long time.

I typed "4% rule" into the search bar and fell into a hole that took about six months to climb out of.

A Financial Planner in 1994 Had an Idea

Here's the origin story nobody in the FIRE community bothers to tell, because it's less exciting than the gospel they've built on top of it.

In October 1994, a financial planner named William Bengen published a paper in the Journal of Financial Planning. Not exactly beach reading. He asked a deceptively simple question: if a retiree withdrew a fixed percentage of their portfolio in year one, then adjusted that dollar amount for inflation every year after, what's the highest percentage that would have survived every 30-year period in modern US market history?

He back-tested rolling 30-year periods from 1926 to 1992. He ran the numbers through the Great Depression, through World War II, through the stagflation hellscape of the 1970s when inflation hit 13.5% and your money was melting in your pocket. He tested portfolios of 50% stocks and 50% bonds, then adjusted the ratios.

The answer he landed on: 4%.

Withdraw 4% of your portfolio in year one. Adjust that dollar amount for inflation every subsequent year. In every historical 30-year period he tested, the money survived. Sometimes barely. Sometimes with a pile left over. But it survived.

A couple of years later, three professors at Trinity University in Texas -- Philip Cooley, Carl Hubbard, and Daniel Sabin -- ran a similar analysis with broader parameters. Their paper, published in 1998, became known as the Trinity Study, and it basically confirmed Bengen's findings with more data and fancier tables. The 4% rule graduated from one guy's research paper to canonical truth.

And that's where the problems start.

The Word Nobody Wants to Say

The Trinity Study didn't say 4% was safe. It said 4% had a 96% success rate over 30-year periods with a 50/50 stock-bond portfolio. Which sounds great until you think about what 96% means.

It means it failed 4% of the time.

If you gathered 25 retirees in a room, each following the rule to the letter, one of them ran out of money. And that one person didn't get a do-over. They didn't get a notification that said "your historical back-test has entered the 4th percentile, please adjust." They just woke up one morning and the account was empty.

The 4% rule doesn't say you won't run out of money. It says you probably won't run out of money. "Probably" is doing a staggering amount of heavy lifting in that sentence.

The FIRE community has a strange relationship with this number. Walk into any Reddit thread, any podcast, any Facebook group where people are plotting their escape from cubicle life, and 4% is discussed with the reverence typically reserved for religious texts. People build their entire lives around it. They calculate their "FIRE number" -- annual expenses times 25, because 25 is just 100 divided by 4 -- and treat it as the finish line. Cross it and you're free.

I did this. I am not above it. My spreadsheet had the number circled in red. But I had questions that the faithful didn't seem to be asking.

The 30-Year Problem

Here's the thing nobody mentions at the FIRE meetups: Bengen designed the 4% rule for someone retiring at 65.

A 65-year-old needs their money to last 30 years. That gets them to 95, which covers the vast majority of lifespans. The math was built for that window.

I quit at 43. If I'm lucky -- and the men in my family tend to be stubborn about dying -- I need this money to last 50 years. Maybe 55.

The difference between 30 years and 50 years in portfolio survival math is not trivial. It's not even linear. Every additional decade introduces more exposure to sequence-of-returns risk -- the terrifying possibility that a major market crash in your first few years of retirement permanently cripples your portfolio, even if the market recovers later. A 30% drop in year two is survivable over 30 years. Over 50 years, with 50 years of inflation-adjusted withdrawals ahead of you? The math gets tighter than a fist.

Some researchers have re-run the numbers for longer time horizons. Wade Pfau, a retirement income researcher, found that for 40- and 50-year retirements, a safer withdrawal rate might be closer to 3.5% or even 3%. The cushion thins. The margin for error narrows.

So I'm sitting at my kitchen table in San Miguel, staring at these numbers, and the voice in my head -- the one that sounds like every HR director I've ever met -- is saying: See? You should've stayed. You should've kept working. The math doesn't support this.

And then I actually ran my own numbers. And the voice shut up.

My Actual Numbers

Let me lay this out, because specifics matter more than theory and I'm not a financial advisor -- I'm a guy at a kitchen table with a spreadsheet and a view of the Parroquia.

Portfolio at retirement: ~$650,000

The 4% rule says: withdraw $26,000 in year one. That's $2,167 per month.

My actual monthly expenses in San Miguel de Allende: ~$2,100 for a family of three.

On paper, the 4% rule fits my life almost exactly. Twenty-six grand a year, and I spend twenty-five-two. But that's only the story if I were living off the portfolio alone, with no other income, rigidly withdrawing exactly 4% adjusted for inflation every single year regardless of what the market did.

That's not how I live. That's not how anyone with a functioning brain lives.

Two adjustments turned the math from "tight and terrifying" to "comfortable enough to sleep through the night."

Adjustment #1: Geographic Arbitrage

Before San Miguel, our monthly nut in the US was approximately $6,800. That's rent in a mid-tier city, a car payment, insurance, groceries at stores that charge nine dollars for a block of cheese, and the general ambient cost of being American. Not extravagant. Not poor. Just... normal.

At $6,800 a month, I'd need $81,600 a year. Apply the 4% rule and you get a target portfolio of $2,040,000. That's the FIRE number for an average American family of three. Two million dollars. Most people see that number and close the spreadsheet forever.

But in San Miguel? $2,100 a month. That's $25,200 a year. Target portfolio at 4%: $630,000.

Same family. Same three humans eating the same three meals a day. But one lives in a place where a beautiful apartment costs $1,200 instead of $2,800, where dinner for two with wine runs $45 instead of $120, where you don't own a car because you don't need a car.

Geographic arbitrage isn't a hack. It's the single most powerful lever in early retirement math. Moving to a place where your money goes three times further is mathematically equivalent to tripling your portfolio.

My $650K portfolio, supporting a $2,100/month lifestyle, puts my actual withdrawal rate at 3.88% -- already under the 4% line before I even get to the second adjustment.

Adjustment #2: Flexible Spending

The 4% rule, as designed, assumes robotic rigidity. You withdraw the same inflation-adjusted amount every single year, no matter what. Market drops 30%? Same withdrawal. Economy enters a recession? Same withdrawal. Your portfolio just lost six figures on paper? Same withdrawal.

Nobody does this. Nobody should do this.

Real humans adapt. In a bad market year, you eat at home instead of going out. You skip the weekend trip to Guanajuato. You buy the 40-peso mezcal instead of the 180-peso one. You tighten, because you can feel the belt, and because you're not an algorithm -- you're a person who reads the news and adjusts.

Research backs this up. Michael Kitces and Jonathan Guyton have both published work on variable withdrawal strategies -- approaches where you reduce spending after bad market years and allow modest increases after good ones. The survival rates for these flexible approaches over long time horizons jump dramatically. We're talking 98-100% success rates over 40+ years.

The reason is intuitive: the scenarios that kill the 4% rule are the ones where the retiree keeps pulling the same amount from a shrinking portfolio, year after year, mechanically, until it bleeds out. But a retiree who cuts back by even 10-15% during a downturn gives the portfolio room to breathe and recover.

I've already done this without thinking about it. Last year, when the market dipped in the spring, we cooked more. I made beans and rice twice a week -- good beans and rice, the kind you learn to make when you live in Mexico and your neighbor's grandmother teaches you. We skipped a trip to Mexico City we'd been planning. Our spending dropped to about $1,800 for two months.

No suffering. No deprivation. Just attention.

The Part That Changes Everything

Here's the number I haven't mentioned yet, the one that makes the whole anxiety about the 4% rule feel slightly absurd in retrospect.

I still work. Not full-time. Not for a boss. Not because I have to. But because I want to, and because the skills I spent fifteen years building in the dot-com world are worth money on the open market. Consulting calls, strategic frameworks, the occasional template that sells while I sleep -- I wrote about this in Building a Business in Your Boxers.

That income -- irregular, self-directed, entirely on my terms -- covers roughly 40% of our monthly expenses. Some months more, some months less. But on average, about $850 a month comes in from work I choose to do.

Which means my portfolio only needs to cover $1,250 a month. That's $15,000 a year. On a $650,000 portfolio, that's a withdrawal rate of 2.3%.

Two point three percent.

The 4% rule was designed for 30 years and it works 96% of the time. The 3.5% rate works for 50 years with near-certainty. And I'm at 2.3%. At that rate, in most historical scenarios, the portfolio doesn't just survive -- it grows. I could potentially leave more to my kid than I started with.

The spreadsheet doesn't just work. It has a margin of error wide enough to park a truck in.

Why the FIRE Community Gets It Wrong

The 4% rule is not scripture. It's a planning tool. A back-of-the-envelope estimate from a financial planner in 1994 who was trying to answer a practical question with historical data.

It has real limitations. It's based entirely on US market returns, which have been historically exceptional -- try running the same analysis on Japanese equities since 1989 and watch the results crumble. It doesn't account for taxes. It assumes a static portfolio allocation that no human actually maintains. It was designed for 30 years, not 50.

But the FIRE community has turned it into an identity. People tattoo "25x" on their foreheads and stop thinking. They treat the number as a destination instead of what it actually is: a rough guardrail on a road that requires constant steering.

The guardrail is useful. You need some framework. You need some number to aim at. Without the 4% rule, the question "how much is enough?" has no answer, and without an answer, most people default to "more" -- which means they work forever, accumulating a pile they're too afraid to spend.

The 4% rule is not a guarantee. It's permission. Permission to believe that enough is a number, not a feeling, and that the number might be lower than you think.

The Real Safety Net

I sleep fine. Not because I've cracked some mathematical code, but because I've stacked enough safety margins that any single failure point can't take us down.

Layer one: A portfolio withdrawal rate under 2.5%, well below the conservative threshold.

Layer two: Geographic arbitrage that makes our money go three times further than it would in the US.

Layer three: Flexible spending that can drop 15-20% in a bad year without any real pain.

Layer four: Earned income from work I'd do for free, covering nearly half our expenses.

Layer five: Skills that are marketable. If everything went sideways tomorrow -- if the market crashed 50% and stayed down for five years -- I could pick up more consulting work within a week. The option to earn is itself a safety net, even when you're not using it.

No single layer is bulletproof. The 4% rule is a guess. My portfolio could take a historic hit. San Miguel could get expensive. Consulting work could dry up. Any one of these things could happen.

But all of them at once? In the same year? While I'm also refusing to adjust my spending?

That's not a plan failing. That's an asteroid hitting.

The Spreadsheet, Revisited

I still open it sometimes. Not at 3 AM anymore -- those days are gone, replaced by a routine that involves coffee at thirty pesos and a walk through cobblestone streets and the slow, unhurried pace of a life that doesn't answer to a sprint cycle.

But every quarter, I update the numbers. Portfolio balance. Spending. Income. Withdrawal rate. I run the projections and check the margins.

It's not anxiety anymore. It's maintenance. Like checking the oil in a car -- except I don't own a car, because I live in a place where you walk everywhere and the biggest financial risk on any given day is buying a second mezcal at dinner.

The 4% rule is a guess. William Bengen would probably tell you that himself. It's an educated guess, backed by a century of market data and validated by decades of academic scrutiny, but it's a guess all the same. It has a margin of error. It has failure cases. It was never meant to be a religion.

But here's what the guess gave me: a framework. A starting point. A number I could plug into a spreadsheet at 2 AM that would tell me, with reasonable confidence, that the life I wanted was possible.

I didn't need certainty. I needed enough certainty to act.

And then I acted. And now I'm sitting in a courtyard in Mexico, writing about withdrawal strategies while the church bells ring and the morning light does that thing it does to the pink stone of the Parroquia, and my wife is reading and my kid is -- still asleep, because some things never change.

The 4% rule is a guess. My life is not. I did the math, and then I did the thing. Perfection is the enemy of freedom, and the spreadsheet was never going to say "go" in bold letters with a guarantee attached. It just had to say "probably."

Probably was enough.

If this resonated, The Dispatch goes deeper every week. More numbers, more stories, no spam.

More Dispatches

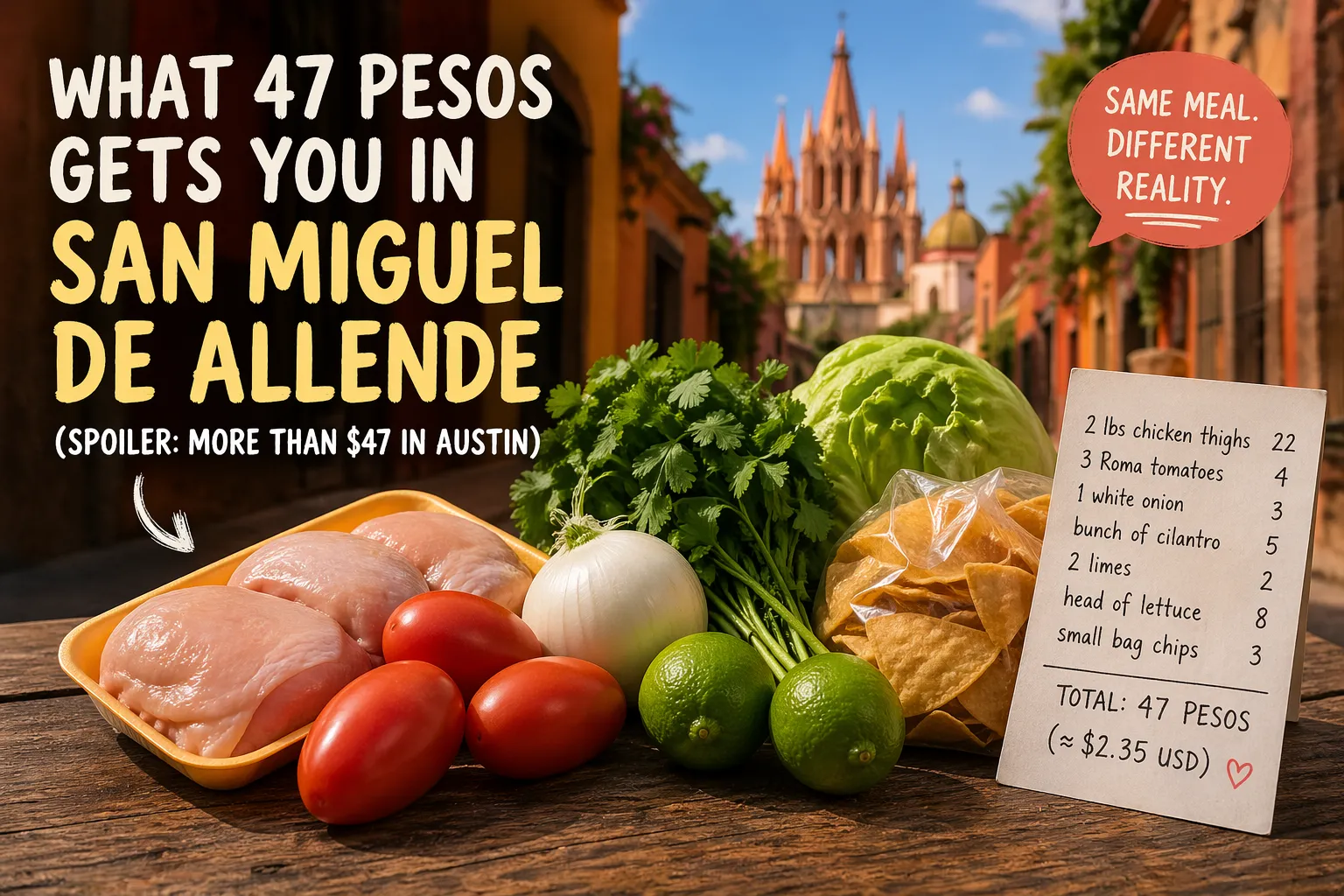

What 47 Pesos Gets You in San Miguel de Allende (Spoiler: More Than $47 in Austin)

I walked into the grocery store with 50 pesos in my pocket — about $2.50 in real money — and came out with enough food for dinner. Not ramen. Not a sad desk salad. An actual meal for three people. This is the kind of math that makes your old life feel like a fever dream. Let me break down exactly what 47 pesos bought me at the local Soriana yesterday: two pounds of chicken thighs (22 pesos), three Roma tomatoes (4 pesos), one white onion (3 pesos), a bunch of cilantro (5 pesos), two limes (2 p

Why I Ignored the 4% Rule (And Retired at 43 Anyway)

The 4% rule is gospel in early retirement circles. Pull 4% from your nest egg annually, the orthodoxy goes, and your money will last forever. Or at least thirty years, which is close enough for most spreadsheets. I ignored it completely. Not because I'm reckless with money — quite the opposite. I spent fifteen years as a corporate finance guy, building models that predicted quarterly earnings to the penny. I know how math works. I also know how life works, and life doesn't follow withdrawal ra