What I'd Tell My 25-Year-Old Self About Money

I wouldn't tell him to invest in index funds. He already knew that. I'd tell him about the three invisible expenses stealing a decade of his freedom.

He was sitting in a Herman Miller chair he didn't own, in an office he didn't like, on the forty-second floor of a building where the elevators smelled like coffee and ambition and dry cleaning. Twenty-five years old, first real job, first real paycheck, first time seeing a number with a comma in it hit a bank account with his name on it.

That was me. And I want to talk to that guy for a minute.

Not about index funds. He'd already read the Bogleheads wiki. Not about compound interest -- he could do the math, at least in theory. Not about the 4% rule or tax-advantaged accounts or any of the mechanical stuff that personal finance blogs love to shout about as if knowing how an engine works is the same as knowing where to drive.

No. I'd tell him about the three things that were about to quietly, invisibly, almost lovingly steal a decade of his freedom. And then I'd tell him the one mental trick that would've made all of it obvious from the start.

He wouldn't listen. Twenty-five-year-olds don't. But I'd tell him anyway.

The Promotion Trap

Here's how it started. I was twenty-seven, and I'd just gotten promoted. Senior something-or-other. The title came with a $12,000 raise and a handshake from a VP whose name I can't remember. I felt like I'd won something.

So I upgraded.

The apartment I'd been renting -- a perfectly fine one-bedroom for $1,200 a month in a neighborhood where you could hear the highway if you opened the window -- suddenly felt insufficient. I was a senior something-or-other now. Senior somethings don't live above a laundromat. Senior somethings have exposed brick and a kitchen island and a building with a name instead of a number.

I found the loft. $2,000 a month. Eight hundred dollars more, every single month, for the privilege of hardwood floors and a doorman who didn't know my name but nodded like he did.

The raise was $12,000 a year. The lifestyle upgrade was $9,600 a year. I'd bought myself a promotion worth $200 a month.

But it didn't stop there. It never stops there. That's the thing about lifestyle creep -- it doesn't announce itself. It doesn't send a calendar invite. It just seeps. The loft needed furniture that matched the loft. The neighborhood had restaurants that charged neighborhood prices. The car I'd been driving -- a sensible used Honda that started every morning and asked nothing of me -- began to feel like a contradiction. A senior something driving that?

I leased a car. Then a better car. Then a better apartment in a better neighborhood to park the better car in front of.

Each raise got absorbed. Every single one. For ten years.

I did the math once, late at night, years after it mattered. The gap between what I needed to spend and what I actually spent, compounded over a decade at 7%, came to roughly $180,000. Not the spending itself -- the opportunity cost. The money that could've been growing, compounding, building the bridge to a life where I didn't need a promotion to feel like I was enough.

One hundred and eighty thousand dollars. Dissolved into hardwood floors and a doorman's nod and a car that depreciated faster than my enthusiasm for driving it.

The apartment didn't make me happier. I know that now. It made me more dependent on the paycheck that funded it. Every upgrade was another bolt in the chain. And I fastened them myself, smiling the whole time, calling it success.

The Invisible Tax

This one is harder to see, because it's designed to be invisible. That's the whole business model.

I never sat down and said, "I'd like to spend $15,000 a year on things I won't remember by Friday." Nobody does. But the machine is built for exactly that.

Here's what $15,000 a year looked like, broken down into charges so small I never noticed them:

Delivery apps -- DoorDash, Uber Eats, the one that lasted three months before it folded -- averaged about $200 a month. Not because I couldn't cook. Because cooking was "too much effort" after a day of aligning deliverables and circling back. The food arrived in bags. I ate it on the couch. It tasted like convenience and mild self-contempt.

Rideshares when a bus existed: $150 a month. The bus was $2.50. The Uber was $14. But the bus required standing, and waiting, and existing in public without noise-cancelling headphones, and I told myself my time was worth more than that. My time, it turned out, was worth exactly $150 a month more than a bus ride.

Subscriptions I'd forgotten about: $100 a month. The meditation app I opened twice. The meal-planning service I never planned a meal with. The premium tier of a music app that sounded exactly like the free tier. The gym membership -- sixty dollars a month -- at a gym I visited twice, both times in January, both times out of guilt.

Amazon impulse buys: $200 a month. A phone charger I didn't need. A kitchen gadget I used once. A book I already owned in a different format. The friction between wanting and having had been reduced to a single thumb tap, and my thumb had no discipline whatsoever.

The lunch delivery because the office cafeteria was "depressing": $250 a month. It was depressing. But $250 a month is $3,000 a year, and the cafeteria had sandwiches that were fine.

Add it up: $960 a month. $11,520 a year. Call it $15,000 once you include the stuff I've blocked out -- the random concert tickets, the impulse gadgets, the "treat yourself" purchases that treated me to exactly nothing lasting.

Over a decade, that's $150,000. Not invested. Not compounding. Not building anything. Just... gone. Converted into Uber receipts and forgotten subscriptions and the mild, temporary satisfaction of not having to try.

These aren't expenses. They're an invisible tax on not paying attention. And the rate is devastating.

None of it was extravagant. That's the cruelty of it. No single charge would make you wince. But stacked up, month after month, year after year, they formed a wall between me and the exit. A wall made of convenience fees.

The Costume

The sneakers cost $400. I remember this because I stood in the store and thought, This is insane, and then I bought them anyway. They were the right sneakers. The ones the right kind of people wore. The ones that said something about taste and status and the particular kind of professional I was becoming.

The backpack was $200. Not because it held things better than a $40 backpack -- it held exactly the same things, in exactly the same way -- but because it was the backpack that people at my level carried. Whatever "my level" meant.

The watch. The jackets. The jeans that cost more than my first week of groceries in San Miguel. I wasn't buying clothes. I was buying a costume. An outfit for the character I was playing in the story of someone who had "made it."

Over a decade, I spent easily $50,000 becoming that character. Fifty thousand dollars on the performance of success.

The irony -- and it took me years to see it -- is that the people who actually "made it," the ones who retired at 42, who walked away from the whole machine and never looked back, were wearing the same five shirts.

They didn't need the costume because they weren't performing. They'd already left the stage.

I was buying an identity because I didn't have one that felt sufficient on its own. The sneakers weren't sneakers. They were proof -- to myself, mostly -- that the hours and the stress and the lost weekends were adding up to something visible. Something you could see.

But you can't wear your way to freedom. And every dollar I spent signaling that I belonged in that world was a dollar that could've been buying my way out of it.

The Letter I'd Actually Write

So here's the letter. If I could fold it up and slide it under the door of that forty-second-floor office where a twenty-five-year-old kid in a Herman Miller chair was depositing his first real paycheck:

You're about to spend the next ten years building a life that requires you to keep building it. Every upgrade, every convenience, every costume piece is another brick in a wall you'll eventually have to climb over. The wall doesn't look like a wall while you're building it. It looks like progress.

The apartment doesn't love you back. The car doesn't know your name. The sneakers will be in a landfill before you're forty.

You're not wrong about the index funds. You're wrong about everything else.

But I know he wouldn't listen. He'd read it, maybe nod, and then open DoorDash because cooking felt like too much effort after a long day. I know this because I was him, and I didn't listen to anyone either.

The Trick I Wish I'd Known

Here it is. The one reframe that changes everything, if you let it.

Stop thinking about money in dollars. Start thinking about it in time.

That $50 dinner? Not fifty dollars. It's an hour and a half of work, after tax. Or -- and this is the version that actually hits -- it's one more day added to the end of your working career. One more day before you're free.

The $800 apartment upgrade? Not eight hundred dollars. It's eighteen more months before you can walk away from the desk and the deliverables and the 11 PM emails from a boss who thinks "alignment" is a personality trait. Eighteen months. A year and a half of your life, traded for a doorman's nod.

The $15,000 a year in convenience spending? That's not an annual expense. That's three to four years added to your sentence. Three to four years of work you wouldn't have to do if you'd just packed a lunch and taken the bus and cancelled the meditation app you never opened.

When you measure purchases in time instead of money, the math becomes unbearable. Beautifully, usefully unbearable.

A dollar isn't a dollar. A dollar is a piece of your life that you traded for it. Spend it like you know that.

This is what the spreadsheet was really telling me that night at 2 AM -- the one I wrote about in The Math That Changed Everything. I thought I was discovering a financial formula. I was discovering a unit conversion. Dollars to time. Expenses to years. The spreadsheet didn't just calculate when I could retire. It showed me how every single spending decision was either buying my freedom or selling it.

If twenty-five-year-old me had done that conversion once -- just once -- on the apartment upgrade, on the car, on the sneakers, on any of it, the whole decade would've looked different. Not because the math is complicated. Because the math is obvious, once you're measuring the right thing.

What It Actually Cost

Three invisible expenses. Ten years. Roughly $380,000 in spending and opportunity cost that didn't make me happier, healthier, or more fulfilled. It made me more comfortable, in the way that a padded cell is comfortable -- soft walls, no sharp edges, and absolutely no way out.

I'm writing this from a rooftop in San Miguel de Allende, where my wife is reading and my kid is doing homework and the Parroquia is catching the last of the afternoon light. Our monthly expenses are about two grand. I own very few things. Almost none of them are impressive.

I have never been richer.

Not because I finally earned enough. Because I finally stopped spending it on a costume, a convenience, and a loft that was really just a very expensive way of telling myself I was doing fine.

If you're twenty-five and something feels wrong -- not broken, just off, like the math isn't adding up even though the paycheck keeps coming -- trust that feeling. You're not crazy. You're paying a tax you can't see, in a currency you haven't learned to measure yet.

Open the spreadsheet. Convert the dollars to days. And then decide -- really decide -- what your time is worth.

I'd tell my twenty-five-year-old self all of this. He wouldn't listen.

But maybe you will.

If this resonated, The Dispatch goes deeper every week. More numbers, more stories, no spam.

More Dispatches

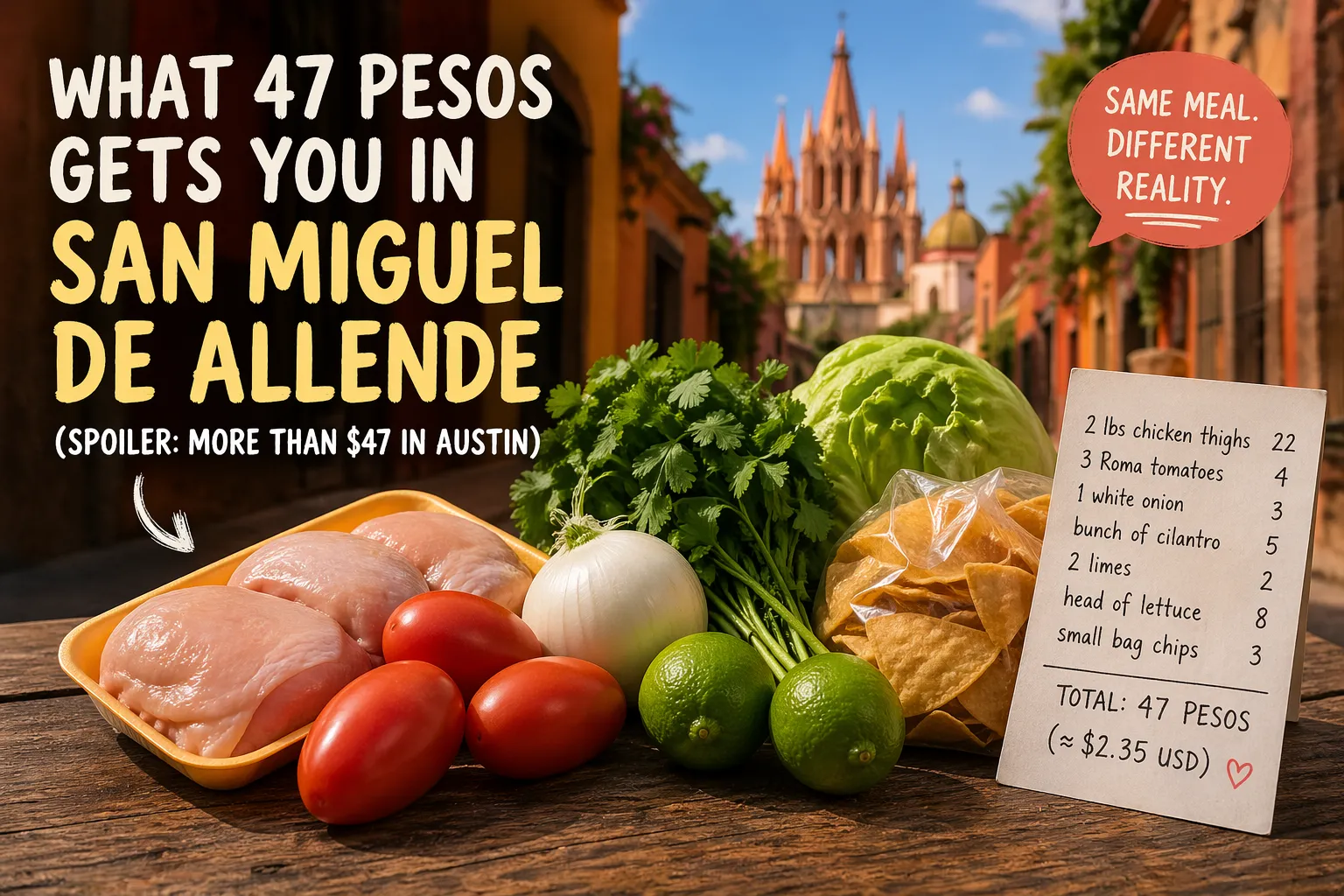

What 47 Pesos Gets You in San Miguel de Allende (Spoiler: More Than $47 in Austin)

I walked into the grocery store with 50 pesos in my pocket — about $2.50 in real money — and came out with enough food for dinner. Not ramen. Not a sad desk salad. An actual meal for three people. This is the kind of math that makes your old life feel like a fever dream. Let me break down exactly what 47 pesos bought me at the local Soriana yesterday: two pounds of chicken thighs (22 pesos), three Roma tomatoes (4 pesos), one white onion (3 pesos), a bunch of cilantro (5 pesos), two limes (2 p

Why I Ignored the 4% Rule (And Retired at 43 Anyway)

The 4% rule is gospel in early retirement circles. Pull 4% from your nest egg annually, the orthodoxy goes, and your money will last forever. Or at least thirty years, which is close enough for most spreadsheets. I ignored it completely. Not because I'm reckless with money — quite the opposite. I spent fifteen years as a corporate finance guy, building models that predicted quarterly earnings to the penny. I know how math works. I also know how life works, and life doesn't follow withdrawal ra