Why I Ignored the 4% Rule (And Retired at 43 Anyway)

The 4% rule is gospel in early retirement circles. Pull 4% from your nest egg annually, the orthodoxy goes, and your money will last forever. Or at least thirty years, which is close enough for most spreadsheets. I ignored it completely. Not because I'm reckless with money — quite the opposite. I spent fifteen years as a corporate finance guy, building models that predicted quarterly earnings to the penny. I know how math works. I also know how life works, and life doesn't follow withdrawal ra

The 4% rule is gospel in early retirement circles. Pull 4% from your nest egg annually, the orthodoxy goes, and your money will last forever. Or at least thirty years, which is close enough for most spreadsheets.

I ignored it completely.

Not because I'm reckless with money — quite the opposite. I spent fifteen years as a corporate finance guy, building models that predicted quarterly earnings to the penny. I know how math works. I also know how life works, and life doesn't follow withdrawal rate formulas.

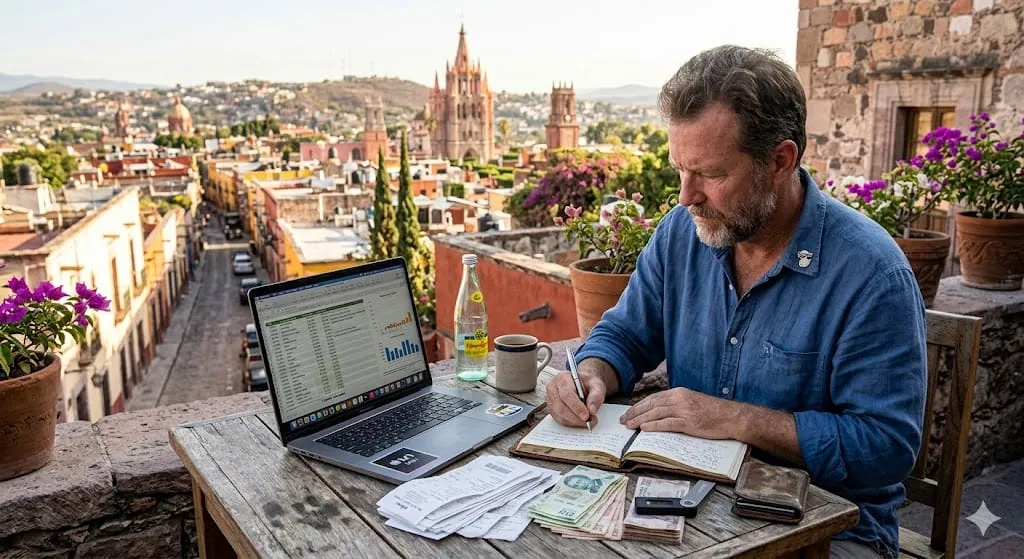

Sitting in my San Miguel de Allende office right now, three years into early retirement, I can tell you exactly why the 4% rule would have kept me chained to a desk until I was fifty-something. And why ignoring it was the best financial decision I ever made.

The 4% Prison

Here's what the 4% rule would have meant for my family: Stay in corporate America until 2031, maybe 2032 if the market hiccupped. Keep grinding through performance reviews and strategy decks and conference calls that could have been emails. Watch my son graduate high school from a cubicle because Dad needed another $300,000 in the portfolio to hit that magic 25x annual expenses number.

The math was tidy. Our annual expenses in suburban Chicago ran about $85,000. Multiply by 25, and I needed $2.125 million before I could safely pull the trigger. At my savings rate, that was eight more years of corporate life.

Eight years.

That's longer than my son had left at home. That's longer than most people stay married. That's longer than the entire Civil War, both world wars, and the Kennedy administration combined.

So I ran different numbers.

The Geography Hack

Here's what nobody talks about in FIRE forums: the 4% rule assumes your expenses stay constant. But expenses aren't laws of physics — they're choices. And some of those choices involve ZIP codes.

My father retired to San Miguel in 1987. Not because he was chasing some expat fantasy, but because his teacher's pension went further here than in Ohio. I'd been visiting this town my whole adult life. I knew what things cost.

Our $85,000 Chicago lifestyle translates to about $45,000 here in San Miguel. Same quality of life — arguably better, since our house has a rooftop terrace overlooking a five-hundred-year-old church instead of a subdivision strip mall. But the numbers changed everything.

$45,000 annual expenses meant I needed $1.125 million at a 4% withdrawal rate, not $2.125 million. Just like that, I'd cut eight years down to two.

But I didn't wait two years either.

The Work-Optional Math

I left corporate at 43 with about $950,000 invested. Not quite enough for the traditional 4% withdrawal, even with our reduced expenses. But enough for something better: options.

Here's the retirement math they don't teach in personal finance blogs. You don't need to replace 100% of your expenses with investment withdrawals. You just need to make work optional. And work-optional happens way before financially independent.

I can pull about $38,000 annually from investments at a sustainable 4% rate. That covers rent, utilities, groceries, and dinner out twice a week in San Miguel. Everything else — travel, the occasional splurge, my son's college fund contributions — comes from the consulting work I do.

The difference? I work because I choose to, not because I have to. Some months I bill forty hours. Some months I bill zero. Last month I turned down a $15,000 project because it would have meant working weekends, and I had plans to explore Guanajuato with my wife instead.

That's not possible when you're optimizing for a withdrawal rate. That's only possible when you're optimizing for freedom.

The Sequence Risk Reality

The 4% rule obsesses over sequence of returns risk — the possibility that early market crashes could derail your retirement. It's a legitimate concern. But there's another kind of sequence risk nobody talks about: the sequence of your life.

What if you spend your forties building the perfect portfolio and your knees give out in your fifties? What if your spouse gets sick? What if your kid needs you during the precise years you're grinding toward that final savings milestone?

I watched my father retire at 65 with enough money to travel anywhere. He chose Mexico partly because it was affordable, but mostly because his body could still handle cobblestone streets and altitude changes. Had he waited until 70 for a bigger nest egg, half the world would have been off-limits.

Retiring "early" at 43 meant I could still hike the mountains around San Miguel with my teenage son. It meant I could lift our suitcases into overhead compartments when we flew to visit family. It meant I could be present for the years that mattered most.

You can't withdraw quality time from a brokerage account.

The Real 4% Problem

The 4% rule isn't wrong — it's just incomplete. It solves for portfolio longevity while ignoring life optimization. It's a formula designed by people who think retirement is a twenty-year vacation funded by stock dividends.

Real retirement — at least the version I'm living — is more complex and more interesting. Some years I'll pull 3% from investments because consulting income is strong. Other years I might pull 5% because I want to take my family to Europe and life is short.

The portfolio will probably be fine. If it's not, I'll adjust. I have skills, I have options, and I live somewhere that expensive mistakes are still affordable.

Most importantly, I have today. Right now, at 3:30 PM on a Tuesday, I'm writing from my rooftop office while church bells ring across the valley. My wife is reading in the courtyard below. My son is at the local university, practicing his Spanish and figuring out his future.

Would this moment be 23% more valuable if I'd waited for that extra $300,000?

I already know the answer. So do you.

The 4% rule would have given me a slightly higher withdrawal rate. Ignoring it gave me three extra years of my life.

I know which math matters more.

If this resonated, The Dispatch goes deeper every week. More numbers, more stories, no spam.

More Dispatches

I Spent 18 Months Tracking Every Peso in San Miguel: Here's What $1,800 Actually Gets You

My spreadsheet has 547 rows. Eighteen months of tracking every peso spent in San Miguel de Allende, from the fifty-peso tip to the woman who waters our plants to the 28,000-peso quarterly property tax bill. Every café cortado, every Uber to the doctor, every bottle of mezcal bought for friends who visit from the States. Why track it all? Because "Mexico is cheap" tells you nothing. Because expat Facebook groups are full of people arguing whether you need $1,200 or $3,000 per month, and nobody

I Spent 18 Months Tracking Every Peso in San Miguel: Here's What $1,800 Actually Gets You

My spreadsheet has 547 rows. Eighteen months of tracking every peso spent in San Miguel de Allende, from the fifty-peso tip to the woman who waters our plants to the 28,000-peso quarterly property tax bill. Every café cortado, every Uber to the doctor, every bottle of mezcal bought for friends who visit from the States. Why track it all? Because "Mexico is cheap" tells you nothing. Because expat Facebook groups are full of people arguing whether you need $1,200 or $3,000 per month, and nobody